Laura Gerhard

Vice President

OVERVIEW

The California almond industry posted shipments of 220 million lbs for the month of November, a 16% decline compared to last year’s 263 million lbs. The shipment number falls in line with market expectations. Exports for the month were down 39.6 million lbs, which is 20% lower than last year. Domestic demand was 65 million lbs, equal to last month, but still off last November’s shipments by 4%. Shipments across all regions now stand at 872.9 million lbs, a 15% decline and 153.9 million lbs lower than last season. Export markets represent 143.8 million lbs of the total decline.

SHIPMENTS

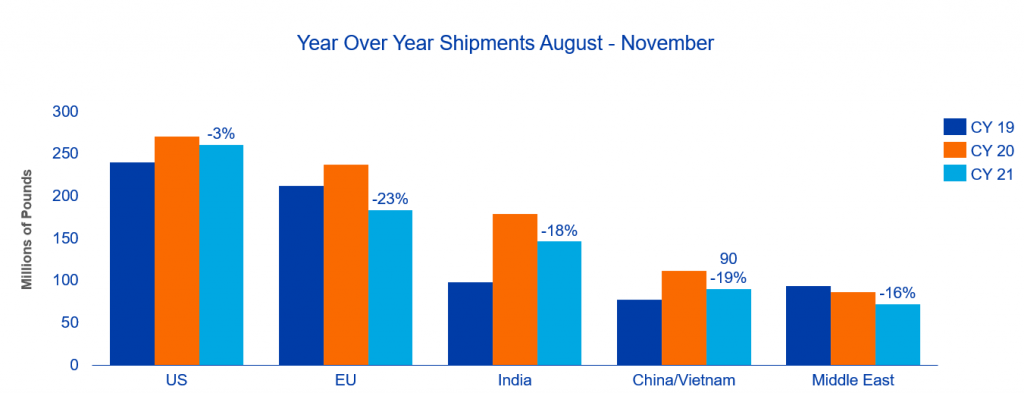

Export shortfalls have continued the same pattern across most major markets. This partly stems from the continued shipping and logistical problems impacting our industry. Shipments that traditionally take less than a month are at times taking 2-3 months to reach export markets, thereby making it nearly impossible to meet export demand. In the Chinese market, these issues have cut at least 6 weeks of potential business leading to a decline of 43% for the month and a year-to-date decline of 17% compared to last year. On the other hand on a year-over-year comparison, Europe fared better in November than October, down 17% and 50% respectively. Europe is now down 23% for the season due to customers pulling old crop through last spring and summer to ensure product will arrive in time for the winter holiday season. On a positive note, both markets will require replenishment in late winter and spring.

Other regions of note include India which continues to be a market for potential despite the market being down 18% year-to-date. The shipment number bodes well for stability in the local market as demand continues to be steady and an early Diwali next year will require product to be sourced out of this year’s supply. The Middle East is up 5% for the month due to strong shipments to UAE, but still down 16% year to date. While smaller markets, Japan and South Korea both posting increases of 19% and 3% respectively.

CROP COMMITMENTS

Total commitments at 753 million lbs are down 252 million lbs and 25% compared to last November. Despite the flurry of activity the past few weeks, new sales for the month came in lighter than most market expectations at 226 million lbs. New sales weighted more heavily in export at 166 million lbs with domestic contributing 60 million lbs, a slowdown from the 105 million lbs in October. Sold and shipped as a percent of total supply is at 49% vs 58% last year. Uncommitted inventory is up 463 million lbs and 59.2% from a year ago. After the first 4 months, the concern remains that the industry is still behind its historical pace and well behind last year’s record numbers. At this point it would be challenging to match shipments from last season, however one could assume the industry still needs to see increased demand. That combined with ongoing logistical challenges, lost consumption in some markets due to vessel delays and higher inventory levels than prior years will continue to put pressure on pricing as the market searches for demand.

HARVEST

Crop receipts for November are trending slightly lower than last year at 2.312 billion lbs versus the prior year of 2.413 billion lbs. While it is too early to make a final determination on the size of this year’s crop it is becoming apparent the crop is likely to be larger than the 2.8-billion-pound NASS Objective Estimate. The next 2-3 months we will provide more clarity in determining the final crop. Storage will become an issue at some point forcing supply to market.

|

Market Perspective Similar to recent months, November shipments have trended below last crop year as nearby demand remains weak with markets adequately covered in the first quarter of 2022. This, along with continued logistical challenges, will continue to weigh on prices in the short-term. Although new sales for the month were thin, there was some encouragement as buyers seemed to leverage nearby price weakness to cover demand in deferred months. This should continue as many global markets look to restock depleting inventories as we move into the new year. One would expect this to provide much needed price stabilization over the coming weeks. Vessel logistics will continue to complicate execution for the foreseeable future. It remains prudent for buyers to purchase needs earlier than anticipated to avoid further complication in their pipelines. Next major milestone for the market will be the almond bloom in February. |

To view Blue Diamond’s Market Updates and Bloom Reports Online Click Here

To view the entire detailed Position Report from the Almond Board of California Click Here